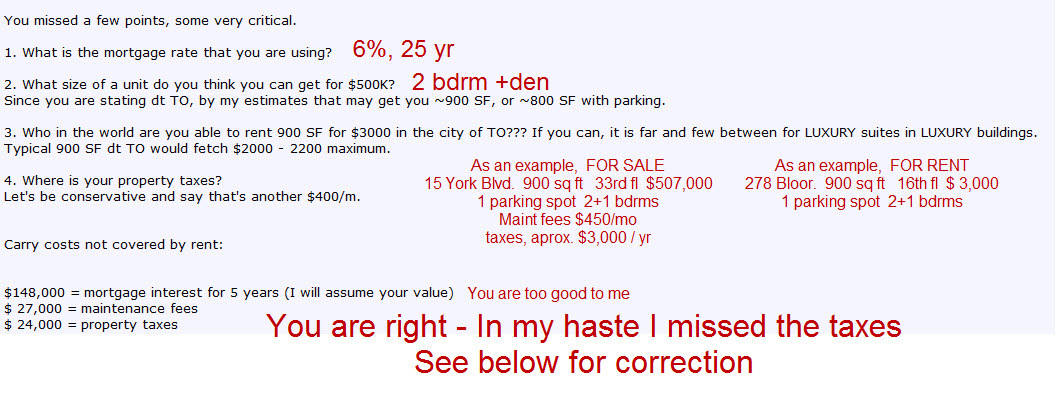

You sound more like a 'Big City Broker' or a perma-bull.

According to the graph you provided:

The first RE recession in 1959 and lasted until 1964 (ie. 5 years); values peaked at $125,000 and dropped 20% to ~$100,000.

There was a burst of 125% growth from 1965 to 1974; but then the next RE recession started and lasted until 1980 (ie. 6 years); then stagnated for another 5 years until 1985, when it sky-rocketed to a peak in 1989 and crashed back down.

In real terms, values dropped 20% from 1974 to 1980; and after the bubble of late 1980s, there was only 5% appreciation over a 22 year span from 1974 to 1996.

Last RE recession occurred between 1989 to 1996 (ie. 7 years) before there was any appreciation in the markets.

During that time, in real terms, values dropped 37% from $400K => $250K; and still HAVE NOT reached their peak after 18 years.

The point is, there is a danger of buying at the peak, which we are at (or just passed depending on your sources).

The "7 to 10 percent or more a year for the past seven years" appreciation you quoted is unsustainable and perpetuated by cheap interest rates.

Since you bring up historical values and trends then use them and not cherry pick. Historical data shows TO values will decline by at least 20%, some say as much as 30% from it's peak.

RE is cyclical ... you probably have at least 4 or 5 years from the peak to buy before there is any uptrend again.

According to TREB "The average GTA price in November 2008 was $368,582. During the same period last year, the Toronto MLS system recorded an average of $393,747". That does not mean prices have dropped $25,000 - Higher priced homes are selling much slower than lower priced homes so the mix is significantly different with a much higher ratio of lower priced homes which brings down the average. A new price index gets around this apples-to-oranges comparison and shows by how much CREA statistics miss the mark. The repeat-sale price index (RSPI), developed by Teranet Inc. and National Bank, says house prices are still above the level of a year ago by 3.3%.

When the average house price is around $320,000 then one should consider buying.

There will be less market risk, still some but less so than currently.

At an average value of $368,582 according to TREB; or $406,741 as referenced by Teranet Inc and National Bank, we are still WAY OVERPRICED and too much risk of being in NEGATIVE equity in the next coming 5 years.